A CD looks simple at first. You deposit money and expect a clear return. The problem shows up when you try to calculate that return. Small details start to change the final number. Rate type matters. Compounding matters. Even the length of the term can shift the result more than expected. A reliable CD calculator clears that confusion. It shows how your money grows step by step, using the same method banks use.

Certificate of Deposit (CD) Calculator

Calculate your CD interest, APY, and growth over time

| Period | Starting Balance | Interest Earned | Ending Balance | Growth |

|---|

The hidden problems with many CD calculators

Not all calculators are built with the same care. Many give quick answers, but they skip details that matter once real money is involved.

Here are a few issues that show up often:

- Some tools treat APR and APY as the same thing

- Others round results too early, which changes the final value

- Short-term CDs get calculated as full-year investments

- Results appear without any explanation behind them

A calculator should not feel like a black box. You should be able to see how each number connects.

A tool that handles more than basic math

This calculator works well for both simple and complex scenarios. It handles short-term deposits, long-term savings, and everything in between.

You can adjust:

- Compounding style such as monthly, daily, or quarterly

- Length of the CD, even if it is not a full year

- Rate type, whether you use APR or APY

It also adapts to different cases. A 3-month deposit will not be treated the same as a 5-year CD. That difference sounds small, but it changes the outcome.

A simple example that shows real growth

Many people trust numbers more when they see a full example.

Let’s take a basic case.

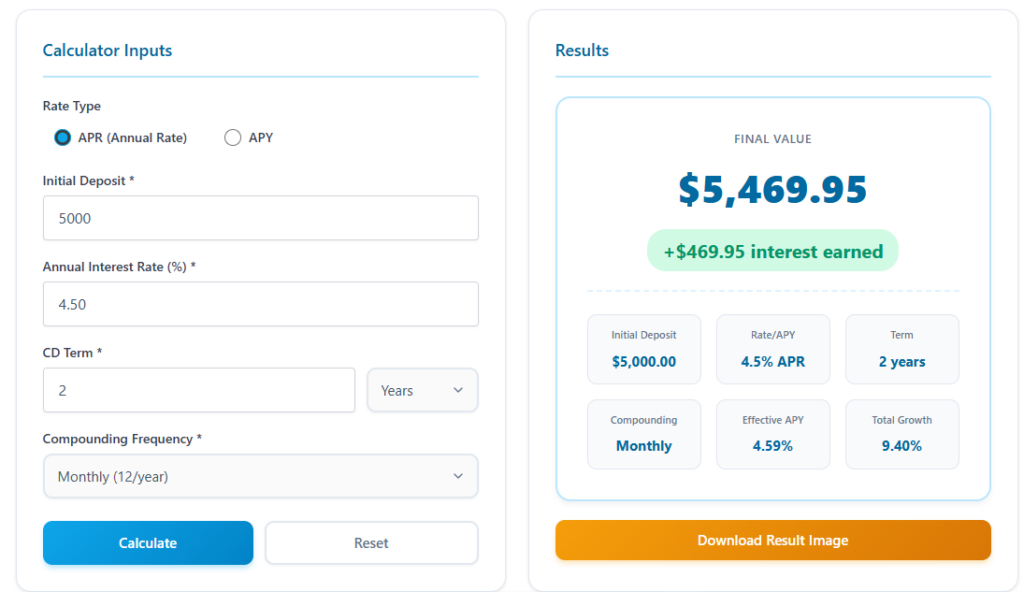

- Deposit: $5,000

- Rate: 4.50% APY

- Term: 2 years

- Compounding: Monthly

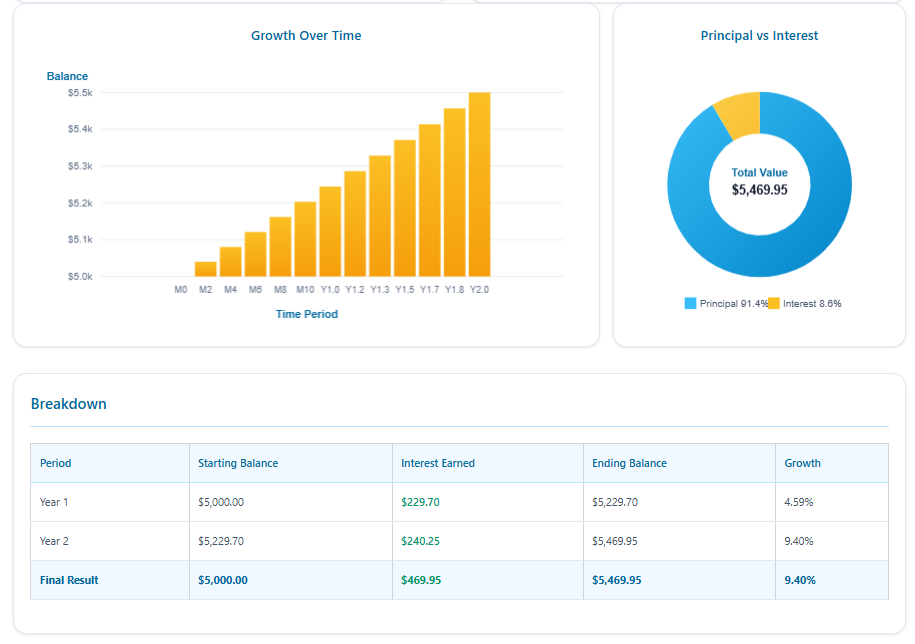

After 2 years, the final value comes close to $5,470.

The interest earned is about $470.

This example shows something important.

The rate looks small, yet the growth builds over time.

Now change one thing and If the same deposit uses daily compounding, the final value goes slightly higher. The difference is not huge in two years, but it becomes noticeable over longer terms. This is why a calculator must reflect real compounding rules.

Why the rate you see is not always the return you get

Banks often highlight APY because it reflects the effect of compounding. APR looks simpler, but it does not show the full picture.

Here is a clear example.

If you invest $10,000 at a 5% annual rate:

- With APR, you see the base rate only

- With APY, you see what happens after interest gets added over time

Monthly compounding increases the final value slightly. Daily compounding can increase it even more. The difference may look minor at first, but it grows over time. This is why a calculator must handle APY conversion correctly. If it does not, the result becomes misleading.

Picking the right CD term without guessing

Choosing a term is not just about the highest rate. It depends on your situation.

Short-term CDs feel safer

- Short terms such as 3 or 6 months give flexibility.

- You can access your money sooner.

- Rates may change, so you can reinvest later.

Long-term CDs lock higher rates

- Longer terms often offer better rates.

- Your money stays fixed for a longer period.

- You earn more interest if rates stay stable.

Read Also: Best CD Term Length Smart Choices Based on Real Timing

Finding the right balance between term and flexibility

A longer CD does not always mean a better outcome. A shorter CD does not always protect you either. The right choice depends on your situation. Time plays a key role. Think about when you may need your money. A long term locks your funds. A short term gives you more control.

Interest rates also matter. Rates can rise or fall over time. A long-term CD may look strong today, but future rates can change. A short-term option lets you adjust sooner. Your comfort level should guide your decision. Some people prefer steady returns. Others want flexibility in case plans change.

A smart approach is to test different options before you commit. Try a shorter term and a longer term. Compare the results. Look at both the final value and the time commitment. A good calculator helps you see both sides clearly.

Small changes in compounding can shift your outcome

Compounding is where many people underestimate their returns.

Think of it this way:

- Monthly compounding updates your balance 12 times a year

- Daily compounding updates it 365 times a year

That means interest builds on itself more often. Over a long period, this creates a visible gap.

Learn More: How Daily Compounding Changes Your CD Returns

For example, a 3-year CD with monthly compounding will end slightly lower than the same CD with daily compounding. The rate stays the same, but the timing changes the result. A reliable CD interest calculator should let you switch between these options and see the difference instantly.

Common mistakes people make with CD calculations

Small mistakes can lead to wrong expectations.

Mixing APY and APR

Some users enter APR and expect APY results.

This creates confusion because APY includes compounding.

Ignoring compounding frequency

Monthly and daily compounding do not give the same outcome.

Many people skip this detail and assume all results are equal.

Trusting rounded numbers

Some tools round values too early.

Even a small rounding error can affect the final result.

Choosing a term without testing options

Users often pick one term and move forward.

They do not compare 1 year vs 2 years vs 3 years.

A proper calculator helps avoid all of these issues.

Read More: APY vs APR CD Difference Real Earnings Explained

Comparing CD offers without guessing

Many savers check multiple banks before choosing a CD. One bank may offer 4.75%, another 5.00%, and a third may change compounding frequency.

Without a proper calculator, it is hard to compare these offers fairly.

You can also check : Common CD mistakes that cost you real money.

With the right setup, you can:

- Enter each bank’s rate

- Match the compounding style

- Use the same deposit and term

- Compare final balances side by side

This gives a clear answer instead of relying on advertised rates alone.

Short-term CDs need careful handling

Short-term CDs are common, especially in uncertain markets. Many people choose 3-month or 6-month options to stay flexible. These shorter periods can cause problems in weak calculators. A tool that assumes a full year will overestimate returns. A tool that ignores compounding timing may underestimate them. A correct approach adjusts everything based on the exact duration. Six months should not be treated like one year. Three months should not be stretched beyond its real timeframe.

Where accuracy really comes from

The formula itself is not the issue. Most calculators use the same base equation for compound interest.

The real difference comes from how that formula is applied.

Accurate tools:

- Convert APY into usable rates properly

- Keep decimals precise until the final result

- Adjust for partial years instead of rounding them

- Use consistent data across charts, tables, and summaries

If one part of the tool shows a different number than another, it breaks trust. Consistency matters just as much as the formula.

Inflation changes what your return really means

A CD can show steady growth. The number looks clean on paper. The real value of that money can tell a different story. Interest alone does not give the full picture. Prices in the economy also move. When prices rise, your money buys less than before.

A quick example

Take a simple case.

- CD return: 5%

- Inflation rate: 3%

Your real gain is closer to 2%.

The rest only keeps up with rising costs.

This gap may look small at first. Over time, it adds up. Long-term deposits feel the impact more than short ones.

Why this often gets ignored

Most calculators focus on interest earned. They show the final balance and total growth. They do not show how much of that growth keeps your buying power intact. Many users see a higher balance and assume strong profit. They do not compare that number with rising prices.

What this means for your decisions

A CD still has value. It protects your savings and offers steady returns. It works well when you want safety and predictability.

Real return depends on two things:

- the rate you earn

- the rate at which prices rise

A CD makes more sense when your rate stays above inflation. The gap between the two defines your true gain. A careful approach looks at both numbers before you commit.

Frequently Asked Questions (FAQs)

A CD calculator estimates how your deposit grows over time. It uses your input such as rate, term, and compounding to show final value and interest earned.

APY reflects the effect of compounding over a year. APR shows the base rate without that effect. APY gives a clearer picture of actual earnings.

More frequent compounding increases the final amount slightly. Daily compounding grows faster than monthly over longer periods.

Short durations such as 3 or 6 months are calculated based on the exact term. The tool adjusts the formula instead of assuming a full year.

Some tools round numbers early or treat rates differently. Accurate calculators keep precision and apply compounding rules correctly.

A CD works best when your goal is stability, not maximum return.